By Hayatte Loukili — Executive Search Director & Energy Transition Market Expert | EnableGreen

Published: 26 March 2026

Battery storage recruitment has become one of the most contested areas in the energy transition. Across Europe, utility-scale battery storage is being financed, developed, and traded as core infrastructure — comparable to transmission lines and grid substations. Capital deployment is accelerating. Policy frameworks are improving. Yet the talent market is not scaling at the same pace. For developers, asset managers, and investors, this is no longer a background concern. It is a live execution risk.

Battery Storage Recruitment: Why the demand signal is structural

The numbers make the case plainly. The EU installed 27.1 GWh of new battery storage capacity in 2025 — a 45% year-on-year increase and the 12th consecutive record year, according to SolarPower Europe. Total installed capacity across Europe now stands at over 77 GWh. Utility-scale systems drove the majority of new installations for the first time, accounting for 55% of all added capacity.

Aurora Energy Research forecasts installed capacity will exceed 80 GW by 2030. LCP Delta projects the figure could surpass 215 GW before the decade closes. Aurora also estimates more than €24 billion flowing into four-hour duration systems alone.

Project scale is moving in one direction. When Fidra Energy — a company that only entered the market in 2024 — announced Europe’s largest battery project at 1,450 MW in the UK, backed by EIG’s Sandbrook Climate Infrastructure Fund, it was not an outlier. It was a signal. Allianz Global Investors acquiring a 50% stake in TotalEnergies’ German BESS portfolio (789 MW, 1,628 MWh, ~€500 million) confirmed the same: BESS is now an established infrastructure asset class with institutional capital behind it.

More projects, more capital, and more complexity — means more senior hiring across every function.

The revenue model is changing and so are the skills required

Early BESS projects were built on contracted ancillary services revenue: frequency response, FFR, and DCR. That model is under pressure. Wood Mackenzie projects that prequalified FCR capacity in Germany will exceed total demand by 2026, and spreads have already narrowed from €120/MWh in 2022 to €80–90/MWh in 2025.

The market is transitioning. Merchant, arbitrage, and hybrid co-location strategies are becoming the commercial foundation for new projects. This is not a problem — it is a maturation. But it changes the hiring brief significantly.

Guillaume Rivron, Managing Partner at Marguerite, frames it clearly:

“The next phase of BESS growth in Europe will be defined by the shift from ancillary services revenue models toward merchant, arbitrage, and hybrid models, underpinned by clearer regulation and accelerated grid investment. Now established as an asset class in its own right, BESS offers diverse risk-return profiles for investors who can master development and procurement, adapt to national market designs, and move selectively and quickly to capture the best opportunities.”

Mastering development and procurement, adapting to national market designs, moving selectively and quickly — these are human capability requirements. They translate directly into specific hiring profiles that the current talent pool struggles to fill at speed.

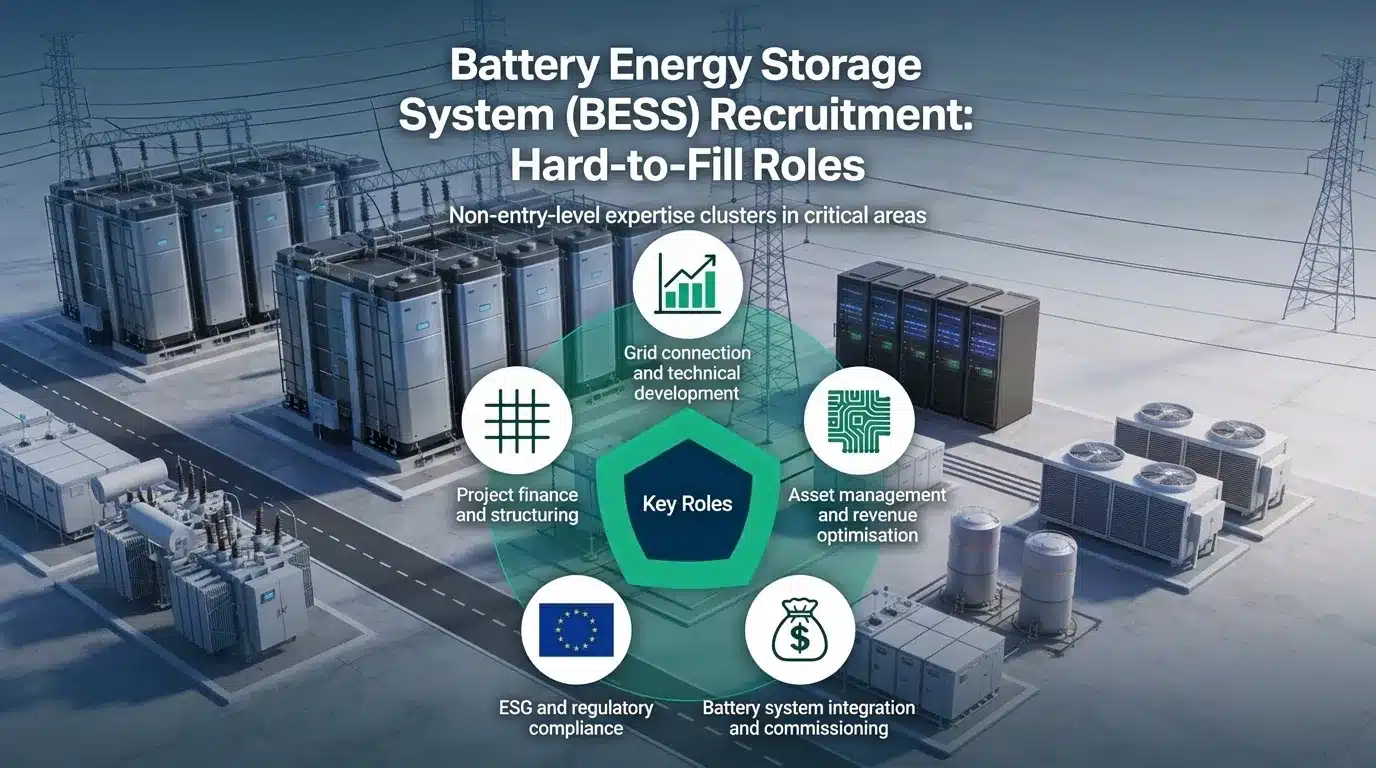

Where battery storage recruitment is hardest

Eighty-two percent of battery industry employers reported shortages of skilled local applicants in 2025, according to the Battery Industry Employment and Talent Needs Assessment (BIETNA). Over 90% of European transmission system operators flagged that skill shortages had delayed grid infrastructure projects. These are not abstract metrics. They describe real project timelines slipping.

The roles with the sharpest supply-demand imbalance in European BESS are:

- Asset managers and revenue optimisation specialists — combining battery dispatch knowledge with power market expertise

- Grid connection and technical development leads — covering permitting, grid code compliance, and TSO interface management across multiple national frameworks

- Project finance and structuring professionals — with BESS-specific experience in merchant risk and infrastructure debt

- Battery system integration and commissioning engineers — bridging power electronics, BMS software, and site safety

- Regulatory and ESG compliance specialists — increasingly critical as the EU Battery Regulation’s Digital Battery Passport requirement takes effect in February 2027

The common thread across these roles is that they sit at the intersection of two or more disciplines. A grid connection lead needs to understand both planning law and power systems. An asset manager needs to model dispatch strategy and negotiate with TSOs. These cross-functional profiles take years to develop — and the BESS sector has only existed at utility scale for five to seven years in most European markets.

There is no legacy workforce to draw from at scale. Professionals are being redeployed from adjacent sectors — power trading, transmission, conventional generation — but the flow of candidates is not fast enough to meet demand.

A practical example: What hiring looks like on the ground

Consider a mid-sized European IPP expanding its BESS portfolio across the UK, Italy, and Poland simultaneously. To execute this, the business needs country-level development leads with jurisdiction-specific regulatory knowledge in each market, a grid connection specialist per pipeline, a senior battery optimisation hire to manage dispatch strategy, and a head of asset management for the operational portfolio. That is five to seven senior hires — in a market where each of those profiles typically has two or three competing offers active at the same time.

The firms winning this competition share common traits. They brief their specialist recruitment partner before the mandate is urgent. They compress the interview process. They make offers decisively — often within 48 to 72 hours of the final interview. Those that don’t are watching project timelines shift — not because of permitting or financing, but because the development team cannot be staffed.

National markets: Where recruitment pressure is most acute

Battery storage recruitment intensity varies by geography, but pressure is building across the board.

The UK remains the most active hiring market for BESS. The pipeline is deep, planning reform is improving, and revenue stacking strategies are more developed than almost anywhere else in Europe. Competition for senior talent — particularly grid, development, and optimisation profiles is fierce.

Germany is the largest storage market in Europe by traded volume, but its regulatory complexity and the ongoing FCR saturation are driving demand for more commercially sophisticated talent, especially in trading and asset management.

Italy and Poland are increasingly attracting capital and developer interest. Both markets face acute shortages of local BESS expertise, which means recruitment often requires international candidates or relocation packages — adding complexity to already competitive searches.

France is expected to become more active from August 2026 following the TURPE 7 tariff reform, which will improve the economics of storage investment significantly.

Author analysis & expert opinion

By Hayatte Loukili, Executive Search Director, EnableGreen

The recruitment constraint in European battery storage is more serious than most market commentary acknowledges. Reports focus on GW pipelines and investment volumes, which are impressive, but rarely capture what is quietly lost in roles that take six months to fill, or never get filled at all.

The most underestimated shortage is not purely technical. It is the commercial-technical hybrid: the asset manager who can model dispatch strategy and present revenue assumptions to an investment committee in the same day. The development director who understands grid code compliance across three national frameworks. These people are not abundant, and they are not available for long when they do come to market.

What concerns me looking forward is that the shift toward merchant and arbitrage revenue models will demand even more sophisticated talent at precisely the moment when existing capacity is already stretched. Developers expanding into multiple European markets simultaneously face compounded complexity — each jurisdiction has its own grid tariff design, permitting logic, and regulatory timeline. Placing a generalist into that context carries real project risk.

The firms that will execute most effectively are those treating battery storage recruitment as a strategic input to their business plan rather than a reactive function. That means engaging partners with genuine sector depth, building talent pipelines before roles are open, and investing in retention as seriously as acquisition.

At EnableGreen, we operate exclusively within the energy transition. Our energy storage recruitment practice covers the full value chain development, grid, finance, asset management, and commercial, across Europe and internationally. We do not place generalists into specialist roles. If you are scaling a BESS team or looking for your next move in this space, explore our current energy storage vacancies or get in touch directly.

FAQ

- What is battery storage recruitment and why is it so competitive in Europe?

Battery storage recruitment refers to sourcing, assessing, and placing professionals in roles across the utility-scale BESS value chain — development, grid, engineering, finance, and asset management. It is highly competitive in Europe because the sector has scaled rapidly while the pool of experienced candidates remains small. Most skilled professionals have two to three active offers at any given time, and average time-to-hire for senior roles is extending. - What roles are hardest to fill in battery storage recruitment?

The most difficult profiles to recruit are asset managers with battery dispatch and power market expertise, grid connection leads with multi-jurisdiction experience, project finance specialists familiar with merchant BESS structuring, battery system integration engineers, and regulatory compliance professionals ahead of the EU Battery Regulation. All require cross-disciplinary skills that take years to develop in a sector that has only existed at scale for five to seven years. - Which European countries have the highest demand for BESS talent in 2026?

The UK leads in both project pipeline volume and hiring intensity, particularly for grid, development, and optimisation roles. Germany has the largest market by traded volume and needs commercially sophisticated asset management and trading talent. Italy and Poland are fast-growing markets where local BESS expertise is scarce, often requiring international recruitment. France is expected to increase activity significantly from mid-2026 following the TURPE 7 tariff reform. - How should energy companies approach battery storage recruitment strategically?

Companies should engage specialist executive search partners before hiring is urgent, streamline interview processes to compress time-to-offer, typically 48 to 72 hours after final stage, and build talent pipelines in advance of confirmed headcount. Investing in employer brand within the BESS community and offering competitive packages benchmarked to current market rates are also critical. Treating recruitment as a strategic input to project planning, not a reactive function, separates the firms that execute from those that fall behind. - Why is battery storage recruitment different from general renewables hiring?

Battery storage recruitment requires a unique combination of technical, commercial, and regulatory knowledge that does not exist in the same depth across other renewables sectors. BESS professionals must understand power market mechanics, battery system technology, grid code compliance, and increasingly complex revenue optimisation strategies. The sector lacks the deep talent legacy that wind and solar have built over two decades, and the pace of growth is significantly outrunning organic candidate development. - How does EnableGreen approach battery storage recruitment?

EnableGreen operates exclusively in the energy transition, with a dedicated energy storage recruitment practice covering the full BESS value chain across Europe and internationally. Mandates span development, grid, engineering, asset management, and commercial roles. The approach is built on genuine sector knowledge — not volume sourcing — which reduces time-to-hire and improves placement quality. Current opportunities are available at EnableGreen Jobs.

Sources & References

- SolarPower Europe — EU Battery Storage Market Review 2025 (January 2026): https://www.solarpowereurope.org

- Aurora Energy Research — European Battery Storage Capacity Forecast 2030: https://www.enlit.world/library/bess-roundup-how-europes-storage-momentum-is-gathering-pace

- Wood Mackenzie — European Battery Storage Deployment 2025 (December 2025): https://www.woodmac.com/press-releases/european-battery-storage-deployment-expected-to-grow-45-year-over-year-to-16gw-in-2025

- LCP Delta — European Energy Storage Capacity Forecasts 2030: https://www.indexbox.io/blog/europes-energy-storage-market-matures-as-focus-shifts-to-project-execution-in-2026/

- Energy-Storage.News — Europe’s Energy Storage Buildout (February 2026): https://www.energy-storage.news/europes-energy-storage-buildout-who-leads-and-who-is-left-behind/

- InnoEnergy — Europe’s Battery Breakthrough Hinges on Skilled Workforce: https://innoenergy.com/news-resources/europes-battery-breakthrough-hinges-on-skilled-workforce/

- BIETNA / Center for Automotive Research — Battery Industry Employment and Talent Needs Assessment: https://www.batterytechonline.com/design-manufacturing/report-battery-industry-needs-more-workers-with-higher-skills

- Marguerite — Guillaume Rivron, Managing Partner (direct quote, 2026)

- LinkedIn / EnableGreen — Why Battery Storage Is Becoming a Core Infrastructure Asset: https://www.linkedin.com/pulse/why-battery-storage-becoming-core-infrastructure-asset-c44yf/